[IrisToolbox] for Macroeconomic Modeling

Stacked time solution method with first-order terminal condition

jaromir.benes@iris-toolbox.com

Overview

- Creating a stacked time system

- Simulation procedure and terminal condition

- Changes in information sets

Model equations

System of \(n\) dynamic conditional-expectations equations

where

- \(n\) is the number of model equations

- \(x_t\) is an \(n \times 1\) vector model variables

- \(\mathrm E_t\!\left[\cdot\right]\) is a conditional expectations operator

- \(k\) is the maximum lag

- \(m\) is the maximum lead

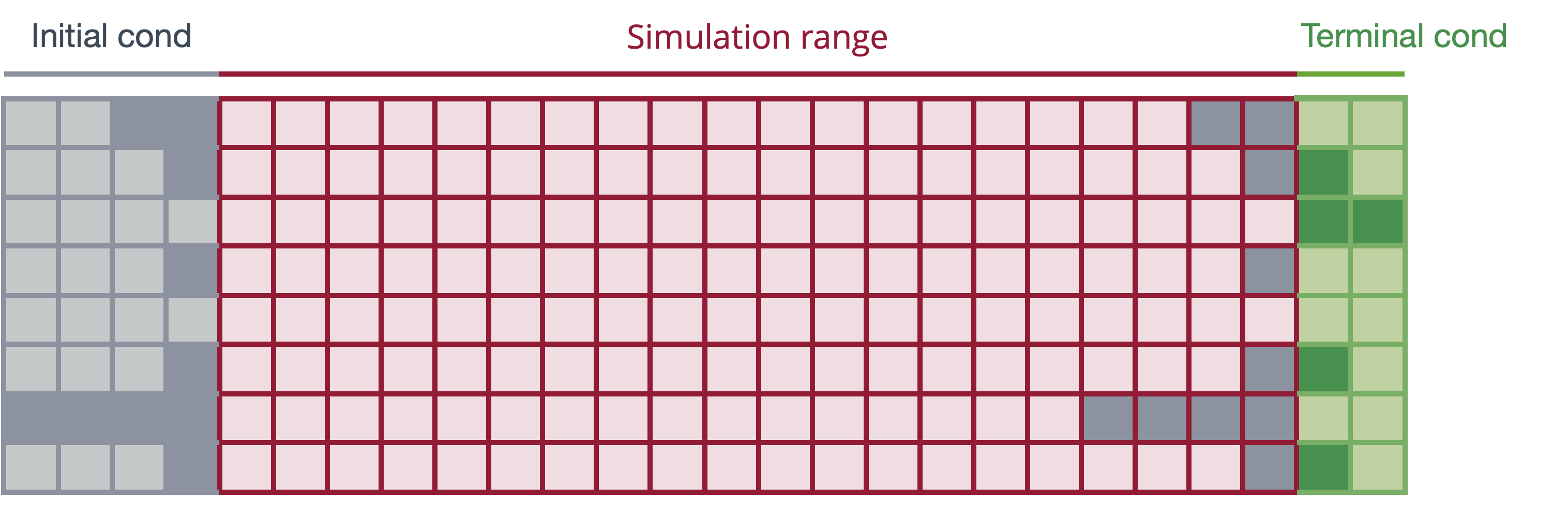

Stacked time setup

-

Simulation range \(t=1, \dots, T\)

-

Drop the expectations operator

-

Stack the \(n\) equations for the \(T\) simulation periods

-

Create a large static system of \(T\times n\) equations in \(T\times n\) unknowns

-

Known initial conditions \(x_{1-k}, \dots, x_{0}\)

-

Unknown terminal conditions \(x_{T+1}, \dots, x_{T+m}\)

Stacked time system of equations and unknowns

- A total of \(n \cdot T\) equations

- A total of \(n \cdot T\) unknows, \(x_t,\ t = 1, \dots, T\)

Simulation setup

Initialize

- Create an \(n\times (T+k+m)\) matrix

- Fill in initial condition in columns \(1, \dots, k\)

In each iteration

- Fill in the simulation range columns

- Taking the last simulation range columns as initial condition, use the first order simulator to fill in terminal codnition

- Evaluate the LHS–RHS discrepancy for all \(n\times T\) equations and send this information to the solver

Visualization of the simulation setup

Terminal condition derived from first-order solution

First-order solution of the model (model-consistent expectations of endogenous variables integrated away)

Create a stacked system to calculate the terminal condition points needed $$ \begin{bmatrix} x_{T+1} \[5pt] \vdots \[5pt] x_{T+m} \end{bmatrix} = T^\mathrm{term} \begin{bmatrix} x_{T+1-k} \[5pt] \vdots \[5pt] x_{T} \end{bmatrix} + K^\mathrm{term} \notag $$

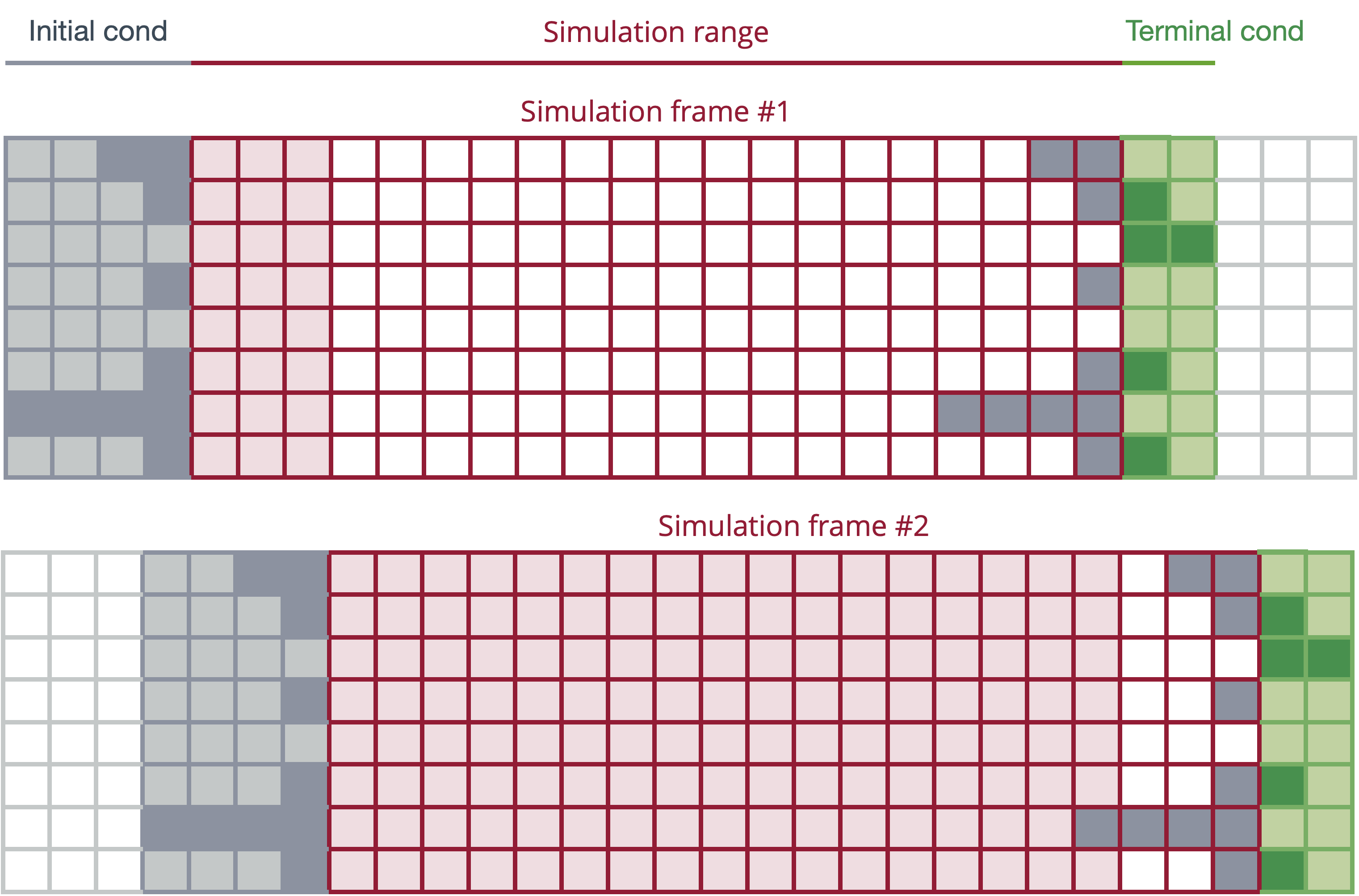

Changes in information sets within a simulation

-

By design, a stacked time simulation is consistent with an assumption of all future events (shocks, swaps) are anticipated

-

To simulate a sequence of unanticipated events, the simulation needs to be broken down into a sequence of sub-simulations (simulation frames)

Breakdown of simulation into frames

Implemenation in IrisT

Syntax of the simulate function for the stacked time method

[outputDb, info, frameDb] = simulate( ...

model, inputDb, range ...

, method="stacked" ...

);

Output structure info

Auxiliary output databank with simulation frames frameDb

Options to control the setup of the stacked time method

startIter=

"firstOrder"(default)"data"

terminal=

"firstOrder"(default)"data"