Iris Toolbox for Macroeconomic Modeling

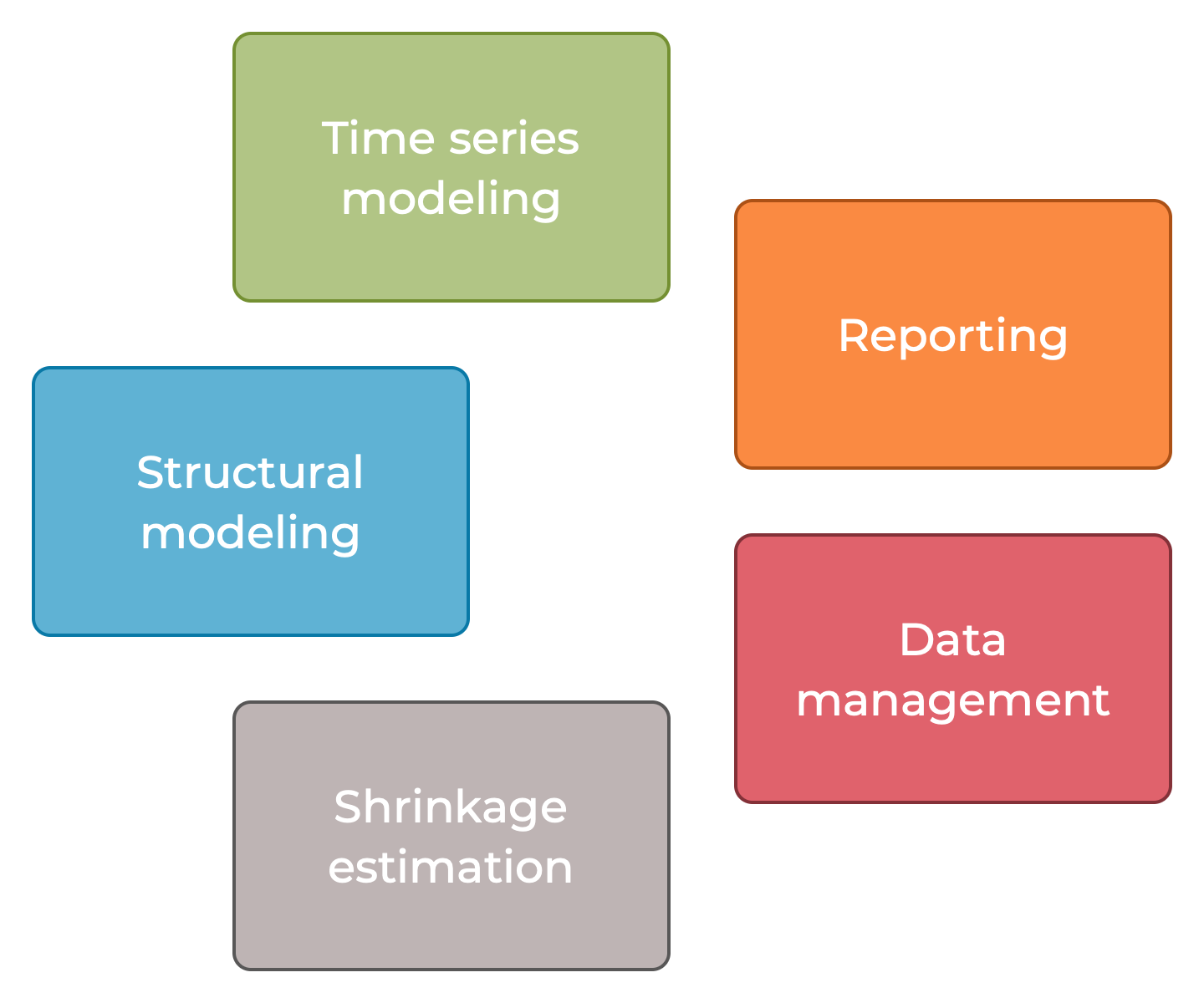

Key functional areas

jaromir.benes@iris-toolbox.com

Overview of structural modeling tools

Develop and operate systems of "structural" equations

-

Model: Structural models including forward-looking nonlinear nonstationary models and DSGEs -

Explanatory: Systems of explanatory equations, including regression equations with ARMA errors, preprocessing and postprocessing equations -

Slang: Iris source language and preparser for writing model source codes with support for multi-file source, source code branching and looping -

Plan: Simulation plans, conditional simulations and forecasts, and model inversions -

+blazer: Steady-state sequential-block analyzer for optimizing the steady-state calculations in large models

Overview of time series modeling tools

Explore shorter-term empirical correlations, deal with the overfitting problem in high-dimensional models

-

VAR: Reduced-form vector autoregressions and panel vector autoregressions -

SVAR: Structural vector autoregressions -

Dynafit: Dynamic factor models -

+x13: Interface to X13-Arima-Tramo-Seats -

Univariate filters for time series objects

Overview of data management

Preprocess and postprocess time series and databanks (structs)

-

Daterand+dater: Dates convenient for evenly spaced periodicities (daily, business-daily, weekly, monthly, quarterly, half-yearly, yearly, integer) -

Series: Time series (dynamic non-frame) manipulation -

+databank: Databanks, batch jobs, import/export from common formats -

Customizable databank serialization to

json,csvformats -

Interface to public database APIs:

+databank.fromIMF,+databank.fromECB,+databank.fromFredpackages

Overview of visualization and reporting

Visualize data on screen and create HTML reports

-

Chartpack: Structured on-screen charting -

+rephrase: Standalone reports based on HTML/JS/CSS/JSON technology -

+visual: Utilities for styling on-screen visualization

Overview of shrinkage estimation techniques

Shrinkage estimators (bayesian)

-

+dummy: Prior dummy observations constructor for "BVAR" estimation -

Posterior: Posterior simulator -

SystemPriorWrapper,SystemProperty,SystemPrior: System prior implementation forModelobjects -

+distribution: Common distribution package